Excerpt from Chapter 4: Fringe Benefits

Economic/Hedonic Damages: The Practice Book for Plaintiff and Defense Attorneys

by Michael L. Brookshire and Stan V. Smith

The definition of fringe benefits is a residual definition.

Fringe benefits are that residual part of the total compensation provided by an employer to an employee, other than such direct elements of compensation as wage and salary, commission, bonus, overtime, and shift differential payments.

Thus, employer contributions to social security; workers’ compensation; unemployment compensation; health, life, and dental insurance; private pension plans; and cafeteria-style benefits plans are among the possible elements of a fringe package.

The proper treatment of employer contributions to employee fringe benefits—as a major element of lost earing capacity and economic damages—becomes more important each year.

At the beginning of World War II, fringe benefits were typically 5 percent of the total compensation provided by employers, even in manufacturing industries. Then began a steady rise in the percentage of payroll, and of total compensation, paid in fringe benefits.

Among the reasons for this trend were the favorable income tax treatment of fringe benefits, for both employers and employees; the influence of both wartime wage controls and labor unions; and the demands of workers themselves for more security against such life “risks” as death, old age with diminished earning capacity, disability, sickness, and unemployment.

Indeed, fringe benefits are intended to provide protection against various life risks.

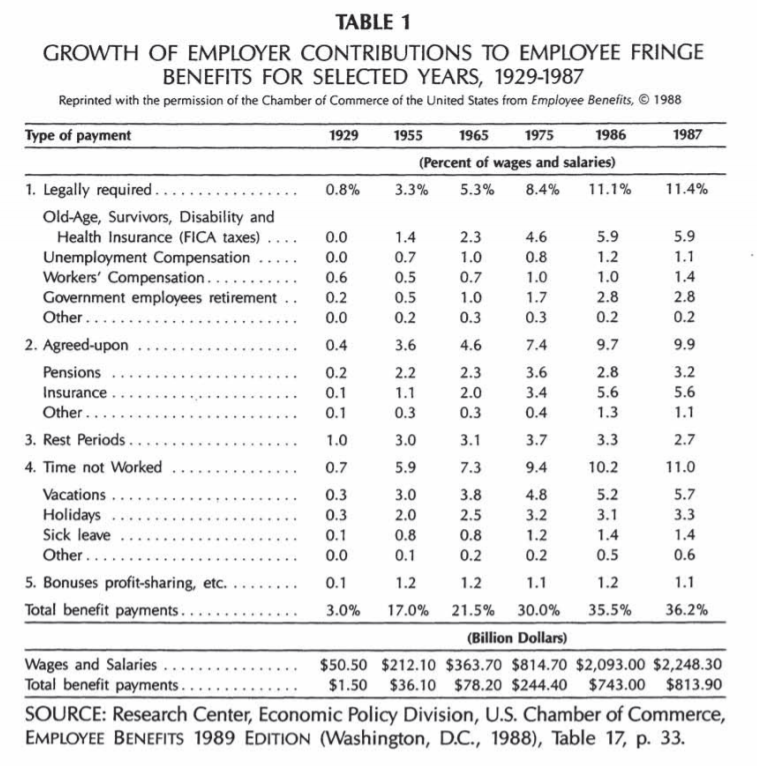

In Table 1 (pictured below), the results of the U.S. Chamber of Commerce survey of average employer contributions to employee fringe benefits are shown for selected years in the 1929-1987 period. These employer-provided fringe benefits, as a percentage of base earnings, rose from 3.0 percent in 1929, to 21.5 percent in 1965, to 36.2 percent in 1987.1

This is an enormous, historical increase in the magnitude of employer fringe benefit payments in relation to the more direct elements of compensation.

On the other hand, the annual increase in this percentage-of-wages figure has clearly declined in the last decade and may have leveled off. By at least one measure in the most recent Chamber of Commerce study, the percentage actually declined from 1986 to 1987, which is the last year measured at this writing.2

As will be explained in more detail later, employer payments such as paid vacations, sick leave, rest periods, lunch periods, and other payments for time not worked must not be included as fringe benefit losses in lost earing capacity estimates, since these payments already show up in annual wage and salary totals.

With this portion of employer payments removed, our experience in relevant fringe benefit payments by employers indicates that the percentage-of-wages employer contribution to fringe benefits is usually in the 20-30 percent range.

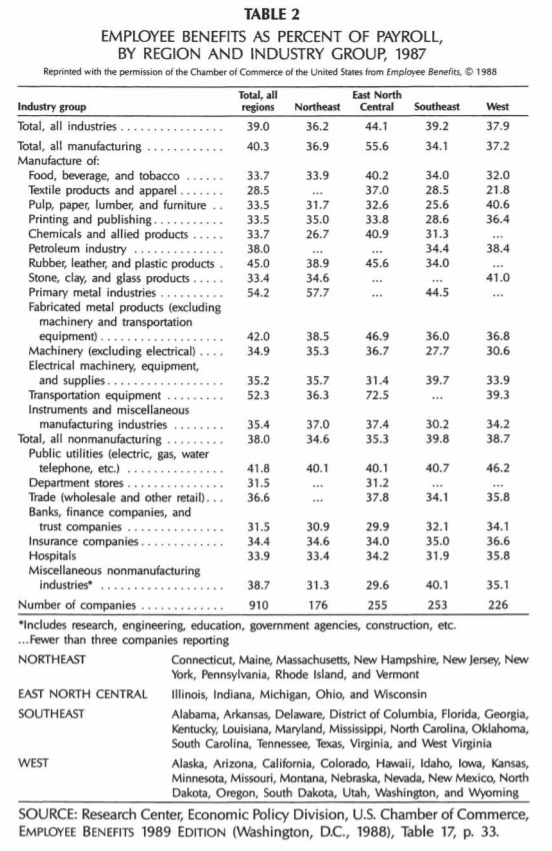

The “statistical class” conclusion about employer contributions to fringe benefits does vary significantly by industry and region, as shown in Table 2. The relevant point is that a wealth of data exists, from the U.S. Chamber of Commerce studies alone, to refine U.S.-wide fringe benefits payments to reflect more specific situations.

For More Information…

- Explore more chapters of the textbook.

- Download Chapter 4 [PDF, 3.85 MB].

Read additional sections from The Practice Book for Plaintiff and Defense Attorneys:

1 – Research Center, Economic Policy Division, U.S. Chamber of Commerce, Employee Benefits 1988 Edition (Washington D.C., 1988), p. 33.

2 – Id, page 5. The average employer payment as a percentage of payroll (excluding benefits for retirees and former workers) declined from 38.3 percent in 1986 to 38.0 percent in 1987. See also Bradley R. Braden, “Increases in Employer Costs for Employee Benefits Dampen Dramatically,” Monthly Labor Review, July 1988, pp. 3-7