Excerpt from Chapter 4: Fringe Benefits

Economic/Hedonic Damages: The Practice Book for Plaintiff and Defense Attorneys

by Michael L. Brookshire and Stan V. Smith

General Approaches to Estimating Fringe Benefits

Most commonly, the estimation of fringe benefit loss is based upon the market theory of loss. Thus, employer contributions to all fringe benefit categories (except paid time off) are measured, because this is the market-determined value of fringes which the employer must provide.

The measurement or estimation process should center upon the fringe benefits being paid on behalf of the specific injured or deceased person. As is true for wage and salary loss estimates, the best approach usually involves the unique history of the individual rather than the averages for large, statistical classes of persons.

Therefore, either the attorney or the economist must obtain fringe benefit information from the last employer, a labor union, or perhaps the plaintiff and his family. The data sought are the exact employer contributions to each category of fringe benefits in the last year of work, or sometimes in the current year, if later.

The amount of employer contribution to each category may be expressed either as a percentage of wage or salary payments or as a dollar contribution per week, month, or year. When it is expressed in dollars, perhaps $150 per month in employer contributions to a family health and dental plan, the dollars may be converted to a percentage of salary in the same year.

Assume the $150 per month, or $1,800 per year, employer contribution in this example and a $30,000 annual salary in the same year. The employer contribution to health and dental plan would be expressed as $1,800/$30,000 or 6.0 percent of salary.

Employer contributions to each fringe benefit category would therefore either be collected as a percentage of annual wages or salary or converted to such a percentage figure. The sum of percentages for each fringe category is the total percentage of employer contributions to fringe benefits.

Typically, this percentage of annual wage or salary earnings is in the 20-30 percent range, but employer contributions to fringe benefits vary widely. They tend to be lower in smaller companies and in the service sector of the economy. They tend to be higher in larger companies, unionized companies, and in the manufacturing sector of the economy.

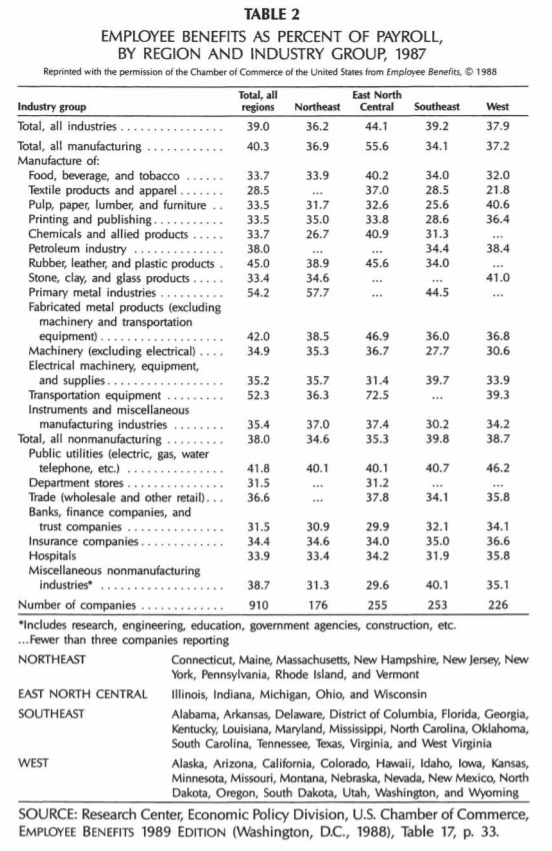

The annual U.S. Chamber of Commerce study captures many of these variations in tables such as Table 2, and useful disaggregations of fringe benefit data, such as hourly versus salaried workers, and part-time workers, are also provided.

Normally, the fringe benefit percentage obtained for the last work year, or perhaps the current year if later, would be used to estimate fringes in all future years. If it were 25 percent, for example, then lost earning capacity in employer-provided fringe benefits would be estimated as 25 percent of the annual wage loss estimate in each year of expected working life.

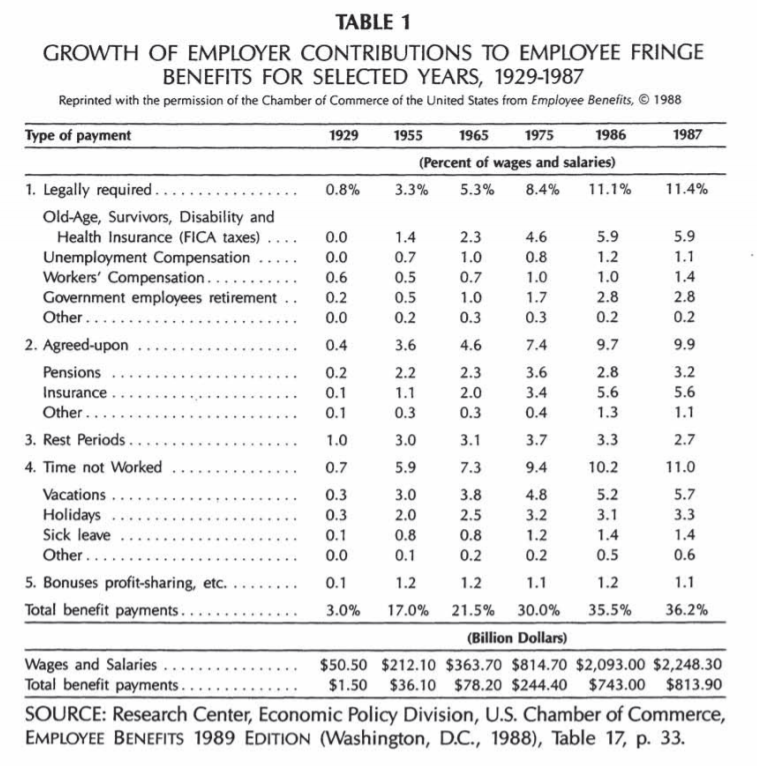

Until recent years, such an approach was considered to be conservative by many forensic economists. As seen in Table 1, the percentage-of-wages figures that represent the value of fringe benefits had been rising dramatically in annual surveys.

A few economists adjusted percentage fringe contributions obtained for a plaintiff in a current year upwards by some trend rate reflecting this historical increase in absolute and relative fringe benefit values.

Table 1 also shows that this upward trend in fringe benefit payments, as a percentage of direct compensation, has leveled. The case for increasing future fringe benefits, based upon a percentage of wages at any future time, is difficult to make, and some forensic economists may argue that the percentage-of-wages contributions will decline.

While forensic economists need to closely watch these trends, for now the best assumption is that currently measured employer payments in fringe benefits, as a percentage of direct compensation, should be frozen when projecting future payments.

Thus, fringe benefit loss estimates would rise with wage loss estimates, based upon the trend rate of annual wage growth, but would maintain the same relative relationship with annual wages in percentage terms.

The “best case” in fringe benefit data collection for a specific individual exists when the employer has provided the employee with a computer-generated benefits statement. Many computer software companies sell the expertise and software necessary for other companies to provide these statements to their employees, and several larger companies have developed the annual statements in-house.

The statements detail annual employer contributions to each category of the fringe benefits provided to that particular employee and show the total employer contributions to fringe benefits for the year. This total, placed over wage earnings in the year, provides the desired percentage figure for the economic expert to use.

The economist does need to ensure that a value for paid vacation, sick leave, holidays, or other paid leave time has not been included.

In a less than helpful situation, neither the attorney nor his client will be able to provide the exact employer contribution to a particular fringe benefit category, either as a dollar amount or as a percentage of wages.

In the least, the economic expert should be provided with those categories of fringe benefits to which the employer contributed. If no work record exists, as in the case of a minor child, assumptions must even be made regarding the categories of fringe benefits to which an employer would contribute.

In either case, a survey of average employer contributions to various fringe benefit categories must be utilized.

Until the early eighties, one such survey was produced by the U.S. Bureau of Labor Statistics. It was sometimes considered to be the “official,” annual survey, as it disaggregated employer percentage payments by fringe benefit categories.

The economic expert was merely required to choose the categories of fringe benefits which he or she felt to be relevant for a particular case and convert the percentage-of-total-compensation figures to percentage-of-wage figures.

Unfortunately, budget cuts in the early eighties forced the federal government to drop this useful statistical series.

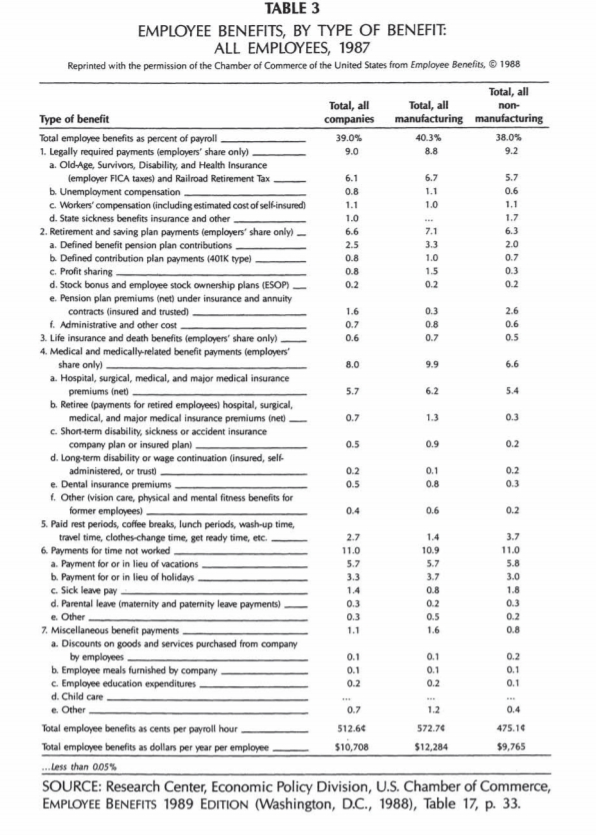

Therefore, the annual survey of employer contributions to various fringe benefit categories, published by the U.S. Chamber of Commerce, is the best available source of current data. Some results of the latest 1988 survey are reproduced in Table 3.

Employer contributions to fringe benefits are expressed as percentages of payroll so that percentages can be directly taken from each relevant category and applied to wage loss estimates for each year.

Assume that a projection of fringe benefit loss was to be made for a person, such as a minor child, with no employment “track record.” The economist would update the 6.1 percent FICA contribution in Table 3 at least to the 7.51 percent employer contribution level for 1989, and the economist should ignore payments for time not worked in categories 5 and 6.

This would produce a figure of 26.71 percent of wages as expected contributions to fringe benefits under the “all companies” column of Table 3.

It should be emphasized again that the 26.71 percent figure can only be used when the LPE reductions, discussed in Chapter 3, have been applied to the wage loss estimates.

Fringe benefit categories relating to the risk of unemployment, sickness, and disability can be properly considered because the wage estimates have been lowered by the probabilities that unemployment, sickness, and disability may lower expected wage-earning in any year. Double-counting does not result.

On the other hand, loss estimates made without LPE reductions should not add these categories in the fringe benefit percentage, or double-counting will result. This would reduce the “all companies” fringe benefit contribution to 22.41 percent of wages for average workers.

The economist must guard against this double-counting problem even when fringe benefit loss estimates are based upon individualized benefits statements or other data specific to a past employer.

As mentioned, the annual U.S. Chamber of Commerce study now provides tables equivalent to Table 3 hourly workers and for salaried workers.

For 1987, the adjusted fringe benefit figure, which is analogous to the 26.71 percent figure derived from Table 3, was 30.0 percent for hourly employees and 26.51 percent for salaried employees.3

In projecting fringe benefit levels for a deceased minor child, the economist need not assume him or her to have been hourly-paid or salaried and should use the less specific table. However, specific percentages from distinct fringe benefit categories in these tables are often used when specific employer contributions only for the category cannot be obtained.

If the deceased or injured worker has been paid on an hourly basis, the fringe benefit percentage for one or more fringe categories can now be taken from a more specific table.

Partial disability cases, where an injured party is still working but in a less remunerative vocation, may offer an additional complication. Some employer fringe benefit contributions, such as social security, are paid as a percentage of wages up to a relatively high annual wage earnings maximum.

Fringe benefit loss is clearly this percentage of the difference between pre-injury and post-injury earning capacity in wages, as long as the pre-injury wages are less than the maximum contribution base.

Other employer contributions, such as those to workers’ and unemployment compensation, are a percentage up to a relatively low wage earnings base. The employer may already be contributing the maximum amount, even given the lower wage earnings of the injured person.

No loss would occur in these categories.

For other categories, loss would occur if no contribution, or a lesser contribution, was being made for a fringe category where some contribution, or a higher contribution, was made in the pre-injury employment.

Of course, it is possible that some post-injury fringes, such as medical insurance coverage, are now better than before, and the loss must be reduced (the overall fringe percentage lowered) to the extent that this is true.

For More Information…

- Explore more chapters of the textbook.

- Download Chapter 4 [PDF, 3.85 MB].

Read additional sections from The Practice Book for Plaintiff and Defense Attorneys:

3 – Id, Tables 4b and 4c are source tables.