Excerpt from Chapter 10: Pre-Trial Tasks and Issues

Economic/Hedonic Damages: The Practice Book for Plaintiff and Defense Attorneys

by Michael L. Brookshire and Stan V. Smith

Defense and plaintiffs’ attorneys seek to reach equitable resolution of their cases.

Most of the time, this pursuit leads to settlement rather than trial. The majority of settlements are reached even before suit is filed, and the majority of the remaining cases are settled before trial.

For both plaintiffs and defendants, there are two principal advantages to settling.

First, the earlier the settlement is reached, the lower the expenses of litigation, both in monetary terms and in terms of the stress of litigation. Second, both sides eliminate the risk of an undesirable verdict.

Settlement depends upon a successful meeting of the minds on a compromise amount. Reaching that compromise depends upon an analysis of many complex factors and successful negotiations.

The important factors include liability issues, the personalities of the parties, the demonstrable nature of the injury, various damage elements, aggravating circumstances, the quality and reputation of the attorneys, jury verdicts in the jurisdiction, the time remaining before trial, etc.

The interplay of these many factors is complex and thus makes the comparison of settlement offers with possible litigation alternatives difficult to assess in purely quantitative terms.

However, the costs of litigating through to a verdict and the risk of an undesirable verdict are such powerful considerations for both sides that, despite the complexity of analysis, settlements are almost invariably reached.

It is beyond the scope of this section to discuss case evaluation procedures and negotiation strategies. While much has been written on these topics, the clients ultimately rely upon the wisdom of their attorneys for this analysis. This wisdom is gained from litigating and settling many cases and from the extensive writings, seminars, and formal legal training in these areas.

The evaluation of a prospective trial result can sometimes be simplified into an outcome matrix showing the weighted average or expected result:

According to this matrix, a litigant should be willing to settle for $1,175,000, but this analysis is, at best, a simple approximation. It does not take into account litigation costs and emotional stresses.

Perhaps most importantly, the undesirability of a poor outcome, which can be different for each side, is not considered. An institutional defendant may be willing and able to suffer a poor outcome.

A plaintiff may have only one chance in a lifetime to achieve financial security and may be unwilling or unable to take substantial extra risk, particularly if a reasonable settlement offer is proposed. Depending upon the parties, the converse may be true in a given case.

Each side will give different weight to these factors, set targets, set first demands and responses, and negotiate.

While estimating an outcome matrix of litigation is complex, the present value of settlement amounts can be successfully analyzed in purely quantitative terms. When settlement negotiations are based on a lump sum amount, the analysis of the settlement value is rather simple. Both sides are discussing offers and counteroffers in terms of a single figure, in present-day dollars.

The analysis of the present value of the periodic payments under a structured settlement, while fairly mechanical, is more complex than the evaluation of a single lump sum. Yet in recent years, the percentage of settlements that involve a structure has increased dramatically and, in fact, such structures lead to more settlements.

This paradox, that a more complicated and difficult-to-value offer facilitates more settlements, is explained by the fact that plaintiffs will place a financial value on the generally tax-free structured payments at an amount greater than the cost to the defendant—a key reason for their increase in popularity.

The original lack of common ground that may have existed in negotiations over a single lump sum can narrow significantly or disappear. There are other sizeable advantages, to both the plaintiff and defendant, for structuring a settlement instead of settling upon a lump sum. There are also disadvantages, and these must be weighed carefully before agreeing to a structure.

The actual cost to the defendant of funding the structure is usually not revealed to the plaintiff. Instead, a present value figure is given. Usually the defendant claims that this preserves the plaintiff’s tax advantage by precluding constructive receipt of the annuity, but this claim is groundless and incorrect.

The principal advantage of not revealing the cost is preservation of the possibility that the plaintiff will value the payments at an amount higher than the cost. While the present value of the payments should be evaluated by the plaintiff independent of the cost, knowing the cost is an important factor in negotiations. Preserving plaintiffs’ attorneys should seek to determine the exact cost as well as any non-standard assumptions about life expectancy.

Defense attorneys, by withholding cost information, may strengthen their position, but they run the risk of being perceived as acting in bad faith.

In some states, the cost must be disclosed. Defense attorneys should always obtain several quotes for the annuity prices since, as for any product, prices can vary substantially.

Based on total dollars paid over time, the value of the payments can appear to be much higher than the highest settlement figure sought by the plaintiff. However, these periodic payment amounts must be discounted to present value, which is a fairly straightforward process.

Plaintiffs; attorneys can then “reality test” their value estimate by seeking to obtain a quote for the annuity from an issuer. The analysis process, while straightforward, is complex and typically requires the expertise of an economist.

While plaintiffs and defendants may not be able to agree on a compromise lump sum payment, the difference in the perceived value of the structured settlement, due primarily to the tax-free status of such payments, is one major reason it serves well to for the common ground in settlement negotiations, even when the costs are known to both sides.

There are other reasons for which structured settlements are more advantageous than the alternative of an identical lump sum award. These are discussed below.

The Nature of Structured Settlements

A structured settlement is one in which payment of part of the settlement amount is deferred beyond settlement day. Hence the settlement calls for periodic, or structured, payments.

The variety of structures is virtually infinite since payments are usually geared to take into account the particular cash flow needs of the recipient.

In most structures, a significant portion of the total funds is pain on the settlement day, and periodic amounts (usually monthly or annually) are paid throughout the balance of the life of the recipient. The periodic payments are usually constant but may grow over time.

However, actual indexing for inflation is rare. Additional lump sums are often scheduled at certain intervals in future years. The periodic payments are typically guaranteed for a minimum number of years, at little incremental expense given the relevant life expectancy tables.

While this section discusses periodic payments principally in the context of personal injury litigation, structured settlements can be used in a variety of settings that seek to obtain the advantage of deferral of payments, including the buyout of business partners, the dissolution of a marriage, contributions to charities, etc.

Taxes

Allocation of lump-sum awards and structured payments can significantly affect the taxes paid by the plaintiff, defendant, insurers, and the plaintiff’s attorney. The governing tax laws are complex and subject to change and various interpretations.

The following is only a commentary on certain possible tax considerations. It is NOT a substitute for tax counsel from experts in taxation. Given the complexity of the tax code, it is IMPERATIVE to seek advice and interpretation from such experts to assure proper conformity to applicable laws, regulations, and revenue rulings, and to obtain the best possible tax advantage.

Payments for personal injuries or sickness and certain other claims for workers’ compensation and other statutory matters are generally free from federal taxes under Internal Revenue Code Section 104(a) (26 U.S.C. §104[a]). This exclusion does not require the filing of a lawsuit.

Payments for contractual injuries, injuries to business reputation and certain other types of claims, however, are generally taxed. Awards are also generally taxable to the extent of reimbursement for deducted medical expenses in the past. Future medical expenses incurred may be deductible only to the extent that they exceed the award for such expenses.

In the past, the IRS distinguished between compensatory and punitive damages, holding punitive damages taxable, although Section 104 does not distinguish between the two types of damages. The tax-exempt status and future deductibility of punitive damages is, at the moment, uncertain.

In general (and within reason), it is desirable for tax purposes to allocate as little as possible to medical expenses, punitive damages, and injury to business reputation.

Conversely, it is desirable to allocate as much of the award as possible to lost income, pain and suffering, emotional harm, and to business property with sufficient remaining eligible basis to offset the award.

Plaintiffs and their expert tax counsel should also examine state laws when deciding upon such allocations. While these allocations are not binding on the Internal Revenue Service (IRS), courts will look to the reasonable nature of such allocations in determining whether they are fair and proper.

Regarding future periodic payments arising from structured settlements, Revenue Ruling 79-220, 1079-2 C.B. 74, authorizes plaintiffs to excluded from their reported income on federal tax returns receipt of payments that are prefunded with an annuity — so long as the transaction is properly configured.

This can represent a distinct advantage since the interest earned on a single lump sum award may otherwise be taxable to the plaintiff unless most of the payments were later offset by tax-deductible future medical expenses, for example.

The existence of tax-free, high-grade securities reduces the size of the tax advantage to some degree, depending upon the actual future tax bracket of the plaintiff and the rate of return on the bonds, but the advantage still remains significant. The tax-free advantage of structured settlements (as opposed to the taxable nature of the interest earned on a lump sum award), is a principal reason this vehicle is desired by plaintiffs and their attorneys.

Plaintiffs can frequently achieve their own tax-free status without a structure, although generally at a sacrifice of investment returns over those that accrue from tax-free, structured settlement annuities.

In determining the allocation of taxable and non-taxable portions of periodic payments, it is desirable to allocate as much as possible to the nontaxable claims and to allocate the awards for taxable claims to more distant future payments.

Spreading reimbursements for previously deducted medical expenses over the years can also reduce the effective tax rate. Financial planning in this regard can bring about substantial tax savings and should be sought. Of course, the allocations are subject to IRS challenge.

The deductibility of the award by the defendant is not set forth in any specific code provision. The general test for deductibility is whether the expense and obligation arose out of conducting an income-producing activity. The desire to reduce publicity or to protect certain assets from claims does not support deductibility.

Rather, it is the actions which gave rise to the claim, the nature of the claim, and whether the claim resulted from ordinary operations. There are further limitations to the 1986 Tax Reform Act which limit immediate tax deductions.

Punitive damages may not be ordinarily deductible but might be deductible if the facts support the deductibility of the compensatory elements of the award. Thus, there appear to be opportunities in drafting the settlement to provide maximum tax advantage to defendants.

In general, when the liability for damages falls upon the insurer, all payments may be deducted, since these obligations arise out of the insurer’s ordinary operations. When the defendant or its insurer purchases an annuity, it can deduct the obligation currently if certain rules are followed.

The 1986 Tax Reform Act qualified Internal Revenue Code Section 130, which now essentially provides for favorable tax treatment of the income the annuity issuer receives from the sale of annuities to fund periodic payments for physical injuries, sickness, and wrongful death by allowing for the deductibility of the cost of acquiring the funding assets (again, provided certain statutory requirements are met).

The plaintiff’s attorney’s fees are frequently based on the present value of the structure. Courts may hold that such fees must be based on the cost of the structure rather than on some other valuation method.

Attorneys’ fees are often paid from the initial payment, but payments may be deferred in any satisfactory way. For an attorney who is a cash-basis taxpayer, an advantage of deferring fees is that, depending on the marginal tax rate, for deferral may lower the attorney’s tax payments by spreading income and deferring taxes paid on the earnings of such income to future years. This does not apply to an accrual-basis taxpayer.

However, an increase in future tax brackets and the uncertainty of the financial status of the obligor could eliminate this possible tax advantage. Last, deductibility is not available if under the fee arrangement the attorney is deemed to have constructive receipt of the fee.

Typically, the defendant (or his insurer) fulfills the periodic payment requirements by purchasing an annuity issued by an annuity company, although other methods of providing for secure future payments are available. 1

Proper transaction configuration of a structured settlement requires that the defendant or the insurer (not the plaintiff) own the annuity and that the purchase per se not relieve the annuity issuer from responsibility for payments in the event of default.

The Technical and Miscellaneous Revenue Act of 1988 Amendment to Section 130 of the Internal Revenue Code permits the plaintiff to be a secured creditor of the issuer, secured by the annuity.

This provides additional financial security to the plaintiff. Proper transaction configuration is critical to assure conformity with — and to take maximum advantage of — the governing tax rules. Thus, specialized tax expertise in drafting the structured settlement is important and should definitely be sought.

Other Considerations

The settlement, whether simple or structured, is often the most significant financial event of the life of the recipient.

Investment of a simple lump sum in risky but high return securities is attractive because it can possibly increase the plaintiff’s wealth over time. But there is always the risk of considerable loss.

To avoid this risk and to assure proper financial management of settlement funds, plaintiffs’ attorneys frequently think it is important that their client be provided periodic payments over the course of many years.

A structure serves as a safeguard against the client’s own lack of investment expertise, imprudent or fraudulent financial management, the appearance of a “sudden suitor,” and other possibilities of premature dissipation, not only for the incompetent or underage plaintiffs but for many people.

Defined benefit pension plans follow this same logic and provide structured rather than lump-sum payments upon retirement.

The safeguarding of a plaintiff’s wealth through periodic payments is seen as one of the principal advantages of a structured settlement. While the plaintiff can always purchase his own annuity with a lump sum settlement amount, it probably cannot confer the same degree of tax advantage.

Moreover, institutional defendants are often able to purchase the annuity at a substantial wholesale discount and obtain further reductions if the life expectancy of the recipient is impaired. These advantages may be shared with the plaintiff, who can usually only purchase annuities at full retail value.

While plaintiffs would ordinarily wish to invest a lump sum settlement in lower yielding, risk free securities, insurers can more easily diversify their risks, obtain higher returns in riskier securities, and offer more to plaintiffs.

Thus, the discount rate used by plaintiffs to value the structured cash flows will be lower than that used by defendants, especially when after-tax returns are properly determined. Hence the plaintiff’s valuation will be higher than the defendant’s cost assessment before taking the tax advantage into account, and even more so after-tax effects are considered.

Herein lies another principal advantage that structured settlements provide; insurance companies can take on more risk, and thus can expect to earn more, on average, than individual investors. A portion of this incremental return can be shared with the plaintiff in the form of larger payments.

Future payments are infrequently geared to rise with inflation. If inflation decreases over time, the plaintiff “wins,” bit if inflation becomes higher than expected, the actual value of the payments falls and the plaintiff “loses.”

The annuity issuer may have the opposite experience, depending upon the types of securities in which investments are made. The plaintiff can hedge against unanticipated inflation through the purchase of out-of-the-money options on interest rate futures, but this requires complex financial management which vitiates one of the principal features of structured settlements.

The insurer usually has more financial expertise and is more able to invest to hedge against inflation. The Model Periodic Payment of Judgements Act2 recommends inflation-indexed payments. Growth in payments can certainly be arranged, but only at some sacrifice to the initial payment level.

To the disadvantage of plaintiffs, a structure is inflexible; once entered into, it cannot be “cashed out” easily to take care of the emergencies that life sometimes serves up. This inflexibility is the result of the inherent advantage of a structure providing safeguards against premature dissipation. It cannot be avoided without jeopardizing the tax advantages form the lack of constructive receipt of the entire present value of the payments.

Also, while the structure payments may be secured by the annuity and, in general, by the assets of the issuer, the payments are not completely risk-free, as is a lump sum payment. Frequently, the liability of the defendant or its issuer is assigned to a third party which may have a stronger balance sheet than the defendant.

Yet, the analysis of the financial ability of an insurance or an annuity company is a complicated endeavor. A.M. Best and Company and the National Association of Insurance Commissioners provide information regarding the expected financial future of an insurance company.

Highly secure insurance companies have not failed in recent decades, but as private entities, they are as subject to market forces as any other business. Examining the future financial viability of the issuer is of critical importance to the plaintiff.

In summary, the advantage to both sides in seeking a structured, versus a simple lump-sum award can be shared so that everyone benefits.

The defendant typically views a structured settlement in terms of its cost, and the plaintiff may be willing to accept a structured settlement which costs less than a negotiated lump sum award due to the possible tax savings, the safeguarding of wealth, the sharing of higher returns from riskier securities with no management costs, and the sharing of the spread between the wholesale and retail cost of an annuity.

The disadvantages of the inflexibility of cash flows, the lack of sensitivity to inflation, and the risk of default by the insurers must be weighed against the advantages.

Valuation of a Structured Settlement

Even though the cost of an annuity may be known, the value to the plaintiff may be higher than the cost. It is important to compare the value to the plaintiff and weigh this against the alternative of a lump sum payment.

The principal elements in valuing a structure to the plaintiff are the timing and the amount of the cash flows, the interest rates assumed for discounting, and the probability of the recipient surviving through each successive year through the age of 100.

Any deviations from normal life expectancy assumptions must be taken into account. Sometimes the defense agrees to make future payments for required future medical expenses that cannot be known with certainty at the time of settlement.

The estimated future payments at the time of the settlement can be used, but this adds some uncertainty to the settlement value. Beyond this uncertainty, the valuation process is fairly straightforward.

While the process may be mechanical, it is all but impossible to accurately value a structured settlement in present value terms without formal mathematical analysis. Our minds are not geared toward mentally calculating to present value a series of periodic and uneven cash flows further affected by mortality statistics, using a yield curve.

Few people easily grasp that, at 12 percent interest, the present value of $10,000 to be received 24 years hence by a 40-year-old black male plaintiff, if alive at the time, is less than $825.

Computers greatly simplify the valuation process. Each future payment must be discounted to present value using a compound interest (discount) rate. Each payment must be further modified by the probability of payment, which is 1.00 if guaranteed and less than 1.00 if dependent upon the recipient’s being alive at the time of payment.

Once the present value of each of the payments has been determined, these are simply added together to arrive at a total present value.

Many economists take the shortcut of not using year-by-year probability of survival statistics through age 100, but only a single life expectancy statistic. They estimate the value of all payments through life expectancy as if they were guaranteed.

This overvalues payments received after the guarantee period expires but prior to the end of life expectancy. Further, it ignores the value of payments that may be received when life expectancy is exceeded. The net effect of the shortcut has the general effect of overestimating the value of a structure; the greater the age of the plaintiff, the greater the overestimation.3

Sample Valuations

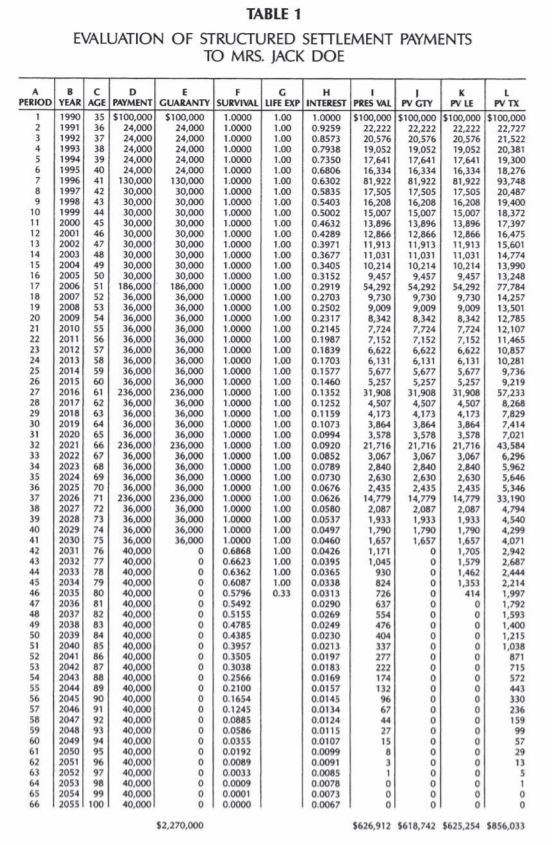

For the purposes of illustration, we assume the following example of payments to Mrs. Doe (wife of Jack Doe, a white female born August 13, 1955) starting August 13, 1990:

$100,000 Cash August 13, 1990

$24,000 per year starting August 13, 1991 for 5 years guaranteed;

$30,000 per year starting August 13, 1996 for 10 years guaranteed;

$36,000 per year starting August 13, 2006 for 25 years guaranteed;

$40,000 per year starting August 13, 2031 through life expectancy but no guaranteed payments if not alive;

$100,000 August 13, 1996 guaranteed

$150,000 August 13, 2006 guaranteed

$200,000 August 13, 2016, 2021 and 2026 guaranteed.

Table 1 shows payments and other statistics regarding the structured settlement analysis as of August 13, 1990. We assume an 8 percent nominal return on risk-free securities. For simplicities sake, we assume a flat yield curve, i.e., interest rates for all government securities are at 8 percent regardless of maturity.

If the yield curve (a graph of the interest rates versus maturity) were not flat, then a separate discount rate for each future year might be used. Yield curves are commonly available from many financial publications.

Assuming a 28 percent marginal tax bracket, the after-tax return for discounting is 8 percent x (100 percent – 28 percent) = 5.76 percent. Further, we assume that Mrs. Doe’s probability of survival is normal for a white female of her age.

The total cash guaranteed (E) is shown to be $2,270,000. While this appears to be a great deal of money, it has a present value at 8 percent discount, affected by guarantees and mortality (l), of only $626,912.

The present value of only the guaranteed payments (J) is $618,742, which is only slightly less than the total present value (l).

If only the guaranteed portion were valued, the structure would be undervalued.

In the sample case, the shortcut of valuing all payments assuming Mrs. Doe lives only to life expectancy (K) also slightly undervalues the true present value. Usually, the shortcut leads to overvaluation.

Any errors resulting in undervaluation increase the probability that the plaintiff may turn down a satisfactory offer.

Errors producing an overvaluation increase the probability that the plaintiff will accept an offer which is financially inadequate. The present value (l) of $626,912 may be somewhat higher than the defendant’s cost, particularly if the annuity company expects to earn more than an 8 percent return on the investment.

However, the perceived value to the plaintiff is a most important consideration since plaintiffs cannot typically earn the same returns without management costs.

When the tax-free nature of payments is taken into account, the perceived present value of the annuity (L) is shown to be $856,033. This figure would be less at lower marginal tax rates.

But at the current rate, the value of the annuity is worth almost $230,000 than a lump sum with interest earnings that are fully taxable. Here, the plaintiff would value the annuity at some $230,000 more than the comparable lump sum award costing the defendant $626,912.

Once the perceived value to the plaintiff is determined, the other factors such as the costs of litigation, the stress of conflict, and the risk of a poor trial result must be weighed to determine the proper course of action; settlement versus trial.

Complex forces are at play in negotiating and evaluating the offer of a settlement, but the important factors described here can be decisive in successfully negotiating a settlement, whether as a simple lump sum or a series of periodic payments.

For More Information…

- Explore more chapters of the textbook.

- Download Chapter 10 [PDF, 4.04 MB].

Read additional sections from Chapter 10 of The Practice Book for Plaintiff and Defense Attorneys:

- General Considerations on the Defense’s Side

- General Considerations on the Plaintiff’s Side

- Discovery Depositions

- Preparations for Trial: Plaintiff & Testimony

1 – Alternatives include various types of trusts, private investment annuities, and court administered funds.

2 – Uniform Law Commissioner’s Model Periodic Payment of Judgements Act (St. Paul, Minnesota: West Publishing Company, 1974 Supplement) ULA Vol. 14.

3 – For a more thorough discussion of this, see STRUCTURING SETTLEMENTS, by Eck and Ungerer, Shepard’s/McGraw-Hill, 198, p. 26.