Alternative Approaches in Selecting Wage Growth Rates Versus Discount Rates

Excerpt from Chapter 3: The Basics of Estimating Wage or Salary Loss

Economic/Hedonic Damages: The Practice Book for Plaintiff and Defense Attorneys

by Michael L. Brookshire and Stan V. Smith

The Concept of The Teeter-Totter Method

A key assumption in lost earning capacity estimates concerns the relationship between wage growth rates and interest (discount) rates.

Once a wage base is established in the trial year, for example, the economist must make an assumption on the rate of wage growth into the future and on the appropriate rate of interest to use in discounting future losses to present values. At trial, we have discussed this relationship in terms of a child’s see-saw, or teeter-totter.

A generalized Teeter-Totter is shown in Figure 1 to illustrate key concepts. Note that the actual wage growth rate is subdivided into its two components of price inflation and real wage growth. The actual discount rate is divided into its sub-components of inflation and the real interest rate.

Examined below are five alternative methods for dealing with the Teeter-Totter in the Jack Doe example.

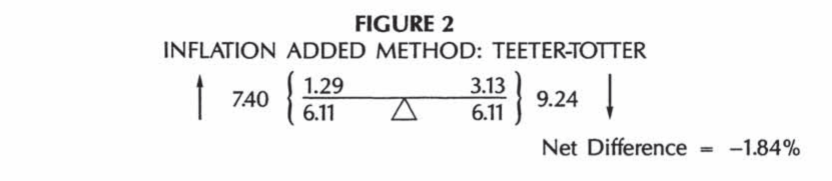

1. Inflation Added Method: Teeter-Totter

Many forensic economists have consistently used this method over the years. As shown in Figure 2, the 1977-1988 average inflation rate of 6.11 percent appears on both sides of the equation.

Actual wage growth is 7.40 percent, or the 6.11 percent inflation rate plus 1.29 in real wage growth. The actual interest rate is 9.24 percent, or the 6.11 percent inflation rate plus the 3.13 percent real interest rate. The critical net difference between 7.40 percent moving upward and the 9.24 percent moving downward is a negative (compounding downward) rate of 1.84 percent annually.

The present value of lost wages is $871,451 under this technique.

2. Inflation Removed Method

This is the method which we have used over the years, except in unusual circumstances.

As shown in Figure 3, price inflation of 6.11 percent is the major component on both sides of the Teeter-Totter. Therefore, the effects of price inflation are canceled out and removed.

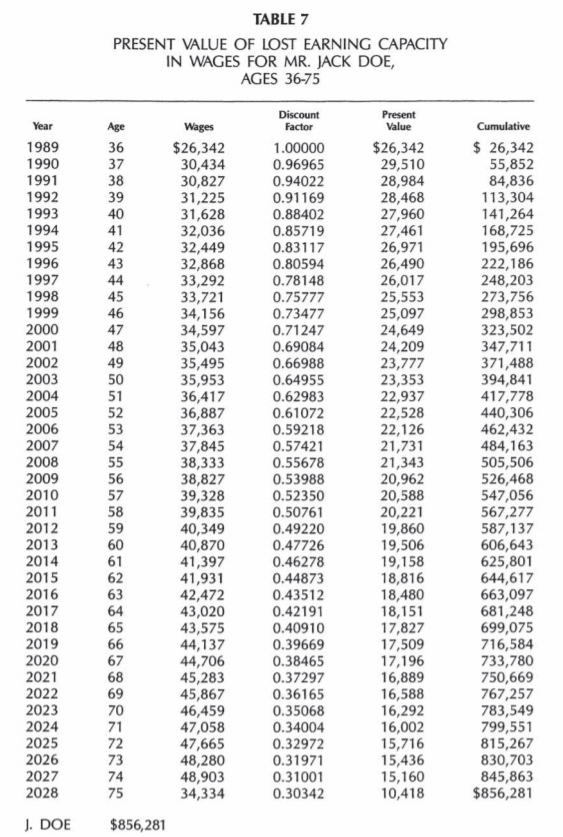

The wage base is increased by Jack Doe’s real wage growth trend of 1.29 percent annually and then decreased to present value at the real interest (discount) rate of 3.13 percent, calculated over the same 1977-1988 period.

The ability of the invested lump sum to cover lost purchasing power of wages is ensured, whatever the rate of price inflation, if the historical relationship between the Teeter side and the Totter side remains basically the same.

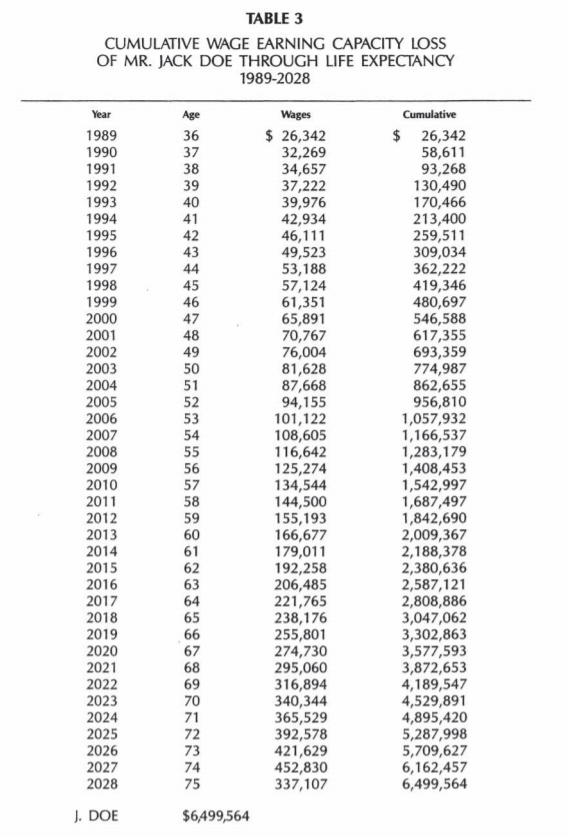

The net difference of 1.84 percent, compounding downward each year, remains the same. Because of a slight mathematical bias when price inflation is removed, the present value of lost wages is lowered slightly to $856,281.

The economist has not needed to predict future rates of price inflation, and the very high wage numbers shown in such inflation-added tables as Table 3 are never calculated or shown. Rather, inflation-removed tables such as Table 7 are shown, annual wage loss numbers look intuitively reasonable, and the emphasis is on the preservation of purchasing power.

3. Total Offset Method

Some have argued that since the net difference may be small in many cases, both components on the Teeter (wage) side should be totally offset by both components on the Totter (discount rate) side.

The advantage of the total offset method is simplicity, in that precise relationships between the Teeter and the Totter are not explained to a jury, and perhaps, the use of an economist can be avoided.

In fact, many other issues must be addressed by an economic expert, so that use of a total offset seldom eliminates the need for a careful examination of economic losses. When a statute or court decision mandates use of a total offset, loss estimates rise.

The net difference is now 0 percent instead of –1.84 percent annually compounding downward (see Figure 4).

In our Jack Doe example, the present value of wage loss becomes $1,188,916, which is $332,635 (or 38.8 percent) higher than the $856,281 inflation-removed estimate.

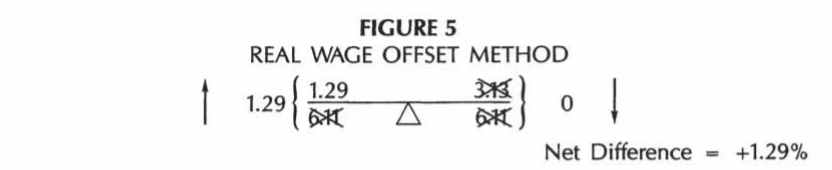

4. Real Wage Offset Method

A handful of jurisdictions have mandated that inflation on the Teeter side be offset against both components—inflation and real interest—on the Totter side. This has an even greater upward effect upon economic loss estimates, as the net difference is the 1.29 percent real wage growth rate (see Figure 5).

This is the only value which has not been canceled out. The present value of wage loss becomes $1,541,207 in the Jack Doe case, or 80 percent higher than the $856,281 estimate in the inflation-removed method.

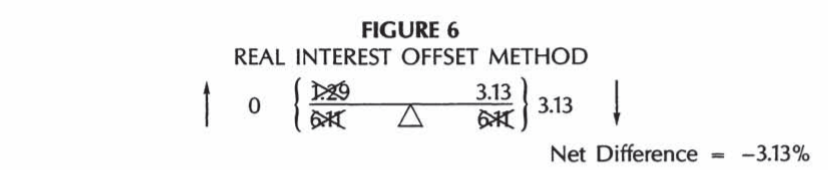

5. Real Interest Offset Method

Finally, a real interest offset might be employed. This is at the other extreme end of the spectrum from a real wage offset.

Both components of wage growth are offset against only inflation on the interest rate side. Only the 3.13 percent real interest rate average would remain so that the wage base would compound downward by the negative net difference of 3.13 percent (see Figure 6).

This method also makes little economic sense.

In the Jack Doe case, the present value of wage loss is $695,015, or 18.8 percent lower than the $856,281 inflation-removed estimate.

In summary, assumptions regarding the Teeter-Totter may make a significant difference in final results.

For More Information…

- Explore more chapters of the textbook.

- Download Chapter 3 [PDF, 7.38 MB].

Read additional sections from Chapter 3 of The Practice Book for Plaintiff and Defense Attorneys: